![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

6, tin ingots

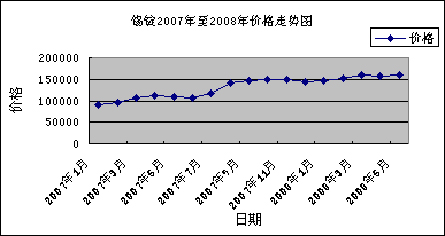

Indonesia is the world's largest tin producer, with an annual output of 120,000 to 130,000 tons of tin, and a global total output of about 350,000 tons. Indonesia's tin production has a great impact on global tin prices. The global tin supply and demand gap in 2007 continued to expand compared to 2006, reaching 21,000 tons. According to ITRI data, in 2007, solder accounted for about 52% of global tin consumption. Asia's tin consumption for soldering accounts for about 80%, and China alone accounts for 55% of the global solder business. In 2007, due to the Indonesian government's reorganization of smelters and small mines, some mines and smelters were closed, resulting in tight global tin supply, leading to rising tin prices. The Indonesian government said it has no plans to restrict tin exports next year, but will continue to improve export management and tin trade on the island to prevent illegal mining of tin mines. At the same time, as can be seen from Figure 6, the price of tin remained firm in 2007, and the price has continued to grow slowly.

In 2008, the world's largest tin supply country, Indonesia, is considering controlling the amount of tin exports. Tin Group said it will limit tin production to support international prices. In 2008, China and Indonesia's exports declined, and output growth was not large. Global demand was relatively stable and there was a slight shortage. China's performance was relatively strong. We predict that the price of tin ingots will rise steadily in the second half of 2008, and there will be no major ups and downs.

| date | January 2007 | February 2007 | March 2007 | April 2007 | May 2007 | June 2007 |

| average price | 91450 | 94830 | 107460 | 111670 | 109530 | 107570 |

| date | July 2007 | August 2007 | September 2007 | October 2007 | November 2007 | December 2007 |

| average price | 117590 | 142360 | 147200 | 150650 | 148860 | 144650 |

| date | January 2008 | February 2008 | March 2008 | April 2008 | May 2008 |   |

| average price | 146980 | 153200 | 159120 | 157480 | 159500 |   |

Figure 6 Price chart of tin ingots from 2007 to May 2008

Second, ferroalloy

1, review 07 market, forecast 08 trend

In order to adapt to the adjustment of industrial structure and promote the upgrading of industrial structure, the country has increased in the past two years.

In the rectification of high-energy-consuming industries, through the establishment of industry access conditions, increase electricity prices, environmental protection requirements, elimination of backward and minimum production restrictions and other mechanisms, comprehensively cooperate with the development of energy-saving emission reduction work. Especially for the ferroalloy industry, the current elimination of iron alloy backward production capacity has been fully carried out, and the export side has also restricted the export of ferroalloy products by increasing tariffs, export license management, and customs price limit measures. Affected by national policies, the ferroalloy market fluctuated greatly in 2007, the ferroalloy output showed a high decline, the proportion of export volume in total production also declined, and the price of ferroalloys increased significantly.

In 2008, the ferroalloy industry will continue to be affected by national policies, showing the following characteristics:

1) Ferroalloy production continued to grow with the increase in crude steel output, but due to the influence of national policies, the growth rate dropped sharply.

2) Ferroalloy imports continue to rise sharply, mainly high/medium/low carbon ferrochrome. As the output of stainless steel increases, the demand for ferrochrome increases, and the price of imported chrome ore is not conducive to domestic ferrochrome production, so ferrochrome imports continue to grow.

3) The export volume of ferroalloys will fall sharply and even lead to negative growth. In 2008, tariffs on ferroalloys were generally raised, and the export of ferrosilicon and silico-manganese was subject to anti-dumping restrictions, which will lead to a decline in China's bulk ferroalloy exports.

4) The ferroalloy market is complex and changeable, and corporate competition is intensifying. In 2008, the prices of some imported products will continue to increase, and the prices of coal, electricity and coke will increase. A series of factors, such as rising seaborne prices, will lead to further increase in the cost of ferroalloys. In addition, the country has adopted a tight monetary policy, and the recovery of payment has slowed down. Production and operation difficulties have increased. Overall prices continue to climb.

2. List some materials analysis

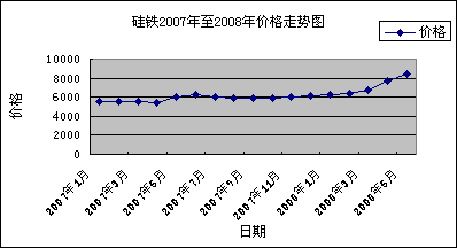

1) Ferrosilicon In the beginning of 2007, the domestic ferrosilicon market was generally stable, at around 5,500 yuan/ton at the beginning of the year. In February, due to the tight road transport and insufficient railway capacity, the transportation cost increased and the market price increased slightly. However, in April, the market price slowly declined. The lowest price in Inner Mongolia fell to 5,460 yuan / ton. After entering May, due to the increase in coal price, the market price of ferrosilicon rose rapidly, and the highest price rose to 6,320 yuan / ton. Since June 1, 2007, the export tariff rate has been raised to 15%, which has a greater impact on the export of ferrosilicon. The export volume has been significantly reduced. Some resources have been transferred from domestic sales to domestic sales. The supply of domestic market resources is more obvious, supply and demand. Contradictions have emerged and prices have gradually declined. However, due to the promotion of cost, especially in the price of electricity and coal, the domestic market price has risen steadily. Until the last trading week in December, the domestic ferrosilicon market price continued to rise slightly. The 75# ferrosilicon factory price in the northwest region was 5800-5900 yuan/ton, and the 72# silicon ex-factory price was 5600-5700 yuan/ton. Moreover, many ferrosilicon export enterprises have suspended their external quotations due to the policy of adjusting the export tariff of ferrosilicon to 25% in 2008, and some manufacturers have increased the export price of ferrosilicon.

See Figure 7: The price of ferrosilicon is still at a high level. First, the European market price has risen to 1,400 US dollars / ton. Although Europe launched the anti-dumping plan for China's ferrosilicon, China's ferrosilicon exports to Japan and South Korea are not losing momentum, and China has increased the management of small-scale ferroalloy plants in China. The strength has made the relationship between supply and demand gradually balanced. Due to the impact of coal price, it is predicted that the price of ferrosilicon will continue to rise in the second half of 2008.

| date | January 2007 | February 2007 | March 2007 | April 2007 | May 2007 | June 2007 |

| average price | 5520 | 5600 | 5600 | 5460 | 6070 | 6320 |

| date | July 2007 | August 2007 | September 2007 | October 2007 | November 2007 | December 2007 |

| average price | 6030 | 5910 | 5913 | 5900 | 6020 | 6140 |

| date | January 2008 | February 2008 | March 2008 | April 2008 | May 2008 |   |

| average price | 6210 | 6310 | 6750 | 7700 | 8450 |   |

Figure 7 Price chart of ferrosilicon from 2007 to May 2008

Previous Next

Cummins Parts,Cummins Spare Parts,Cummins Performance Parts,Original Cummins Parts

JINING SHANTE SONGZHENG CONSTRUCTION MACHINERY CO.LTD , https://www.sdkomatsudozerparts.com