![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

Abstract Stock Code: 300179 Securities Abbreviation: Sifangda Announcement No.: 2013-055 Henan Sifangda Superhard Materials Co., Ltd. About the investment of its own idle capital Debon Innovation Capital Xinghao Capital Starlight Yao 3 (No. 1) special asset management The announcement of the plan is the public...

Stock code: 300179 Stock abbreviation: Sifangda Announcement No.: 2013-055

Announcement of Henan Sifangda Superhard Materials Co., Ltd. on the investment in Debon Innovation Capital Xinghao Capital Xingguangyao Phase III (No. 1) special asset management plan with its own idle funds

Announcement of Henan Sifangda Superhard Materials Co., Ltd. on the investment in Debon Innovation Capital Xinghao Capital Xingguangyao Phase III (No. 1) special asset management plan with its own idle funds

The company and all members of the board of directors guarantee that the contents of the announcement are true, accurate and complete, and there are no false records, misleading statements or major omissions.

I. Overview of foreign investment

1. The Eighteenth Meeting of the Second Board of Directors of Henan Sifangda Superhard Materials Co., Ltd. (hereinafter referred to as “Sifangda†or “Companyâ€) reviewed and approved “Investing in Debon Innovation Capital Xinghao Capital with its own idle funds†The Proposal of Starlight Yao 3 (No. 1) Special Asset Management Plan, agrees that the company will use RMB 10 million to subscribe to Debon Innovation Capital Xinghao Capital managed by Debon Innovation Capital Co., Ltd. (hereinafter referred to as “Debon Innovation Capitalâ€) Starlight Yao 3 (No. 1) special asset management plan share (Class B).

2. The subscription amount accounts for 1.48% of the company's latest audited net assets. It is not subject to the shareholders' meeting for review within the scope of approval of the board of directors.

3. The company has no relationship with Debon Innovation Capital.

Second, the basic situation of investment targets

1. Name of the asset management plan: Debon Innovation Capital Xinghao Capital Starlight Yao 3 (No. 1) special asset management plan;

2. Asset manager: Debon Innovation Capital (the company is a wholly-owned subsidiary of Debon Fund Management Co., Ltd., the legal representative is Yao Wenping, and the business scope is the specific customer asset management business and other businesses licensed by the China Securities Regulatory Commission. Involving administrative licenses, operating with licenses})

3. Asset custodian: China Merchants Bank Co., Ltd. Shanghai Branch;

4. Type of subscription: share of Class B asset management plan;

5. Investment Manager: Ye Bin, Master of Laws, Fudan University, Legal Qualifications, Fund Qualifications, worked in Xinhua Trust Co., Ltd., implemented and managed multiple trust projects, no overdue or bad records, and rich trust practice Experience and excellent risk management skills.

Third, the main content of the special asset management plan contract

1. Asset management plan share classification

The asset management plan share is divided into a class A asset management plan share and a class B asset management plan share. The principal and income distribution order of the class A asset management plan share takes precedence over the class B asset management plan share. During the duration of the asset management plan, the plan does not assign any Class B asset management plan benefits to any principal holding a Class B asset management plan share until all expected benefits from the Group A asset management plan share are realized. .

The investment period for the A-type asset management plan share is 24 months (can be extended for no more than 6 months), and the principal and income are allocated at one time. Class A asset management plan shares are divided into A1 asset management plan share, A2 asset management plan share, and A3 asset management plan share. The amount of single subscription funds is less than RMB 3 million (excluding) for the A1 asset management plan share; the single subscription fund size is between RMB 3 million (inclusive) and 10 million (excluding) for A2 The share of the asset management plan; the size of the single subscription fund of RMB 10 million or more is the share of the A3 asset management plan.

The investment period for the B-type asset management plan share is 36 months (can be extended for no more than 6 months) and the proceeds are allocated within 0-6 months after the investment period expires.

The ratio of the Class A asset management plan share to the total capital of the Class B asset management plan share is between 1.2:1 and 1.4:1.

Investors can simultaneously subscribe for Class A asset management plan shares and Class B asset management plan shares, but the amount of subscription for each type of asset management plan share is not less than 1 million, and each type of shares will be allocated separately according to their respective investment periods.

2. Investment scope

This plan is an asset management plan for a specific purpose. After the plan comes into effect, the asset manager will use the planned property to subscribe for the limited partnership share of Shanghai Xingwei Equity Investment Center (Limited Partnership) or its parallel funds, including but not limited to Shanghai Xinglu Equity Investment Center (Limited Partnership), Huzhou Xingyao Equity Investment Partnership (Limited Partnership), etc., and correspondingly hold the share of the AB limited partnership within the limited partnership invested in the asset management plan. The limited partnership invested is managed and operated by its corresponding original general partner.

The basic situation of the asset manager's investment target:

Shanghai Xingwei Equity Investment Center (Limited Partnership), registered at Room 302, Building 11, No. 728 Lingyan South Road, Pudong New Area, Shanghai, with limited partnership. The general partner of the partnership is Shanghai Xingwei Equity Investment Management Co., Ltd., a limited liability company officially established and validly existing under the laws of China. The registered address is Room 125A, Building 1, 88 Yangxin Road, Pudong New Area, Shanghai. The business license number is 310000000119300. .

Shanghai Xinglu Equity Investment Center (Limited Partnership), registered at Room 110, Building 6, 1499-1, Shangchuan Road, Pudong New Area, Shanghai, with limited partnership. The general partner of the partnership is Shanghai Xinglu Equity Investment Management Co., Ltd., a limited liability company officially established and validly existing under the laws of China. The registered address is Room 109, Building 6, 1499 Shangchuan Road, Pudong New Area, Shanghai. The business license number is 310000000119295.

Huzhou Xingyao Equity Investment Partnership (Limited Partnership), registered at Anji Lingfeng Tourist Resort (in the original heliport), adopting a limited partnership. The general partner of the partnership is Anji Xinghao Equity Investment Management Co., Ltd., a limited liability company officially established and validly existing under the laws of China. The registered address is Anji Lingfeng Tourist Resort (in the original heliport), and the business license number is 33052300006738.

The general partner's subscribed capital contribution accounts for 1% of the total capital contribution of all partners, and is funded in RMB cash. Limited partners: including Class AB limited partners, Class C limited partners. The limited partner shall be liable for the debt of the partnership enterprise to the extent of its subscribed capital contribution.

In order to achieve the purpose of parallel investment, the partnership and parallel funds jointly establish a joint investment entity with limited liability. The partnership and parallel fund will directly or indirectly invest in the invested company through the joint investment entity to obtain the final actual holding right.

3. The purpose and business scope of the partnership

The purpose and purpose of the partnership: the general partner takes the normative and efficient promotion of cooperation and establishes the partnership as the entry point, and diversifies the financial instruments and diversifies the investment method, and establishes appropriate conditions on the premise of fully embodying the strategic intention of equality and mutual benefit. An operational business architecture that enables partners to interact with long-term resources. Jointly develop investment and urban complex operations in the familiar areas of China, especially in the Yangtze River Delta, to create a satisfactory return on investment for partners.

The business scope of the partnership is: equity investment and related consulting services.

A partnership may not engage in the following businesses: absorbing or disguising public deposits; trading in futures and financial derivatives; engaging in unlimited liability; sponsoring and donating (except for unanimous consent of all partners); The sale and purchase of shares of listed companies for the purpose of price difference (except in the following cases: (A) through the unanimous consent of all partners, participation in the listed company to raise funds, or to acquire the listed company for the purpose of controlling the equity of the listed company; or (B) after the listed company is listed, The partnership transfers the untransferred portion or the part of the shares of the company held by the partnership; other business prohibited by laws and regulations.

4. Safeguard measures

(1) The principal and income distribution order of the limited partnership C category limited partnership share is inferior to the class AB limited partner. The ratio of the paid-in capital contribution of the C-type limited partners to the total paid-in capital contribution of the partnership is between 22% and 30%.

(2) Shanghai Xingye Investment Development Co., Ltd. promised: Within 2.5 years from the date of establishment of the plan, it agreed to grant the joint investment entity a liquidity support entrusted loan amount of RMB 500 million. This liquidity support loan is only used to repay the Class A principal of Xinghao III Fund and its income.

(3) The joint investment entity provides a pledge guarantee for the equity of the invested company it holds.

(4) The invested company provides the second-order mortgage guarantee for the land after it acquires the land and the land meets the mortgage conditions.

(5) The Class AB limited partner is a member of the advisory committee of the limited partnership and serves as the chairman of the advisory committee. It has half of the voting rights in the advisory committee (if the voting on the resolution of the advisory committee is 50%: 50% deadlock, then the class AB limited partnership The committee member automatically adds a voting right, and the advisory committee shall vote on the resolution and execute it according to the result of the re-voting.)

5. Income distribution of the partnership

In principle, the partnership is distributed in cash as much as possible. If the project investment cannot be realized or the non-cash allocation is more in line with the interests of all partners based on the independent judgment of the general partner, the general partner may decide to distribute it in a non-cash manner.

(1) Distribution order

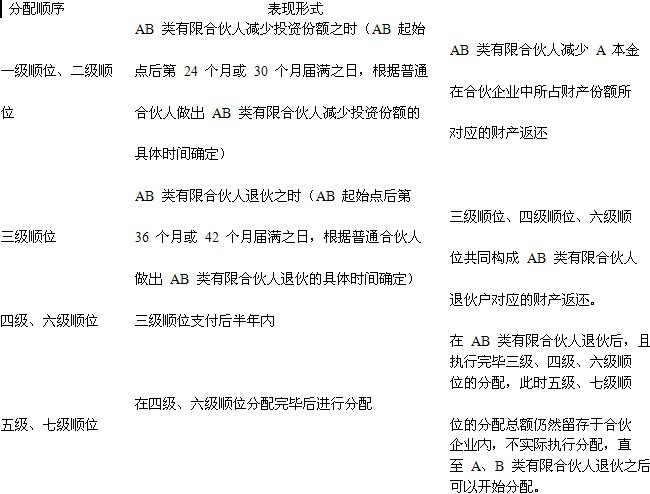

The premise that the ratio of the total paid contribution of the class AB limited partner to the total paid contribution of the partnership is between 70% and 78%. When the partnership is distributed to each partner, the interests of each partner shall be in accordance with Follow the order below:

Level 1 order: assigned to a Class AB limited partner until the Class AB limited partner receives an amount equal to the A principal;

Level 2: Assigned to a Class AB limited partner until the Class AB limited partner receives the basic income of the A principal;

Level 3: Assigned to a Class AB limited partner until the Class AB limited partner receives an amount equal to the B principal;

Level 4: Assigned to a Class AB limited partner until the Class AB limited partner receives the basic income of the B principal;

Five-level order: assigned to the C-type limited partner, general partner, until the C-type limited partner, the general partner obtains the C principal, the general partner's capital;

Six-level order: assigned to the AB limited partner as a floating income when withdrawing from the partnership;

Seven-level order: The distribution of income of the partnership for the C-type limited partners and general partners.

(2) Class AB limited partner income

It is premised that the ratio of the total paid contribution of the class AB limited partner to the total paid contribution of the partnership is between 70% and 78%. The limited partner of the class AB of the partnership shall reduce the share of the property according to the agreement and shall allocate it when withdrawing from the partnership. The total amount is as follows:

i. The paid-in capital contribution of the limited partners of class AB;

Ii. Basic income of class AB limited partners;

“Basic income†means: (1) When the class AB limited partners reduce their share of property, the basic benefits obtained by the class AB limited partners are: reduced paid contribution × annualized rate of return A × AB starting point To the Class AB limited partners to reduce the actual amount of investment (in accordance with the decision of the general partner to determine the time of withdrawal) the actual number of investment days / 365; (2) when the class AB limited partners withdraw from the group, the class AB limited partners obtained The basic income is: the actual contribution amount in the partnership at the time of withdrawal, the annualized rate of return B × AB from the starting point to the withdrawal of the class AB limited partner (in accordance with the decision of the general partner to determine the withdrawal time) Investment days / 365, the same below.

The above “annualized rate of return A†is 11% (expected value, whichever is actual), and “annualized rate of return B†is 10% (expected value, whichever is actual). According to the proportion of the capital contribution of the partnership class AB limited partners and the class C limited partners, the general partner has the right to adjust the annualized rate of return A and the annualized rate of return B.

Iii. Floating income obtained from a partnership when a class AB limited partner withdraws.

When the class AB limited partner withdraws from the partnership, the net asset value of the joint investment entity (assessed in accordance with the provisions of the Limited Partnership Agreement) is deducted from the balance of the above items (1) and (2), minus the limited class C. The residual value of the partner and the general partner after the paid-in capital contribution, the class AB limited partner extracts 30% of the above residual value as the floating income benefit (according to the partnership agreement, the part of the income should also be paid to the general partner) Floating income commission). After the above distribution is completed, the partnership enterprise can allocate to the C-type limited partners and general partners, in accordance with the proportion of the capital contribution of the C-type limited partners and general partners.

The order in which the above orders are allocated in time is as follows:

6, the burden of the trigger point loss responsibility

In the case of a Class AB limited partner reducing the share of the property and making an allocation in accordance with the Limited Partnership Agreement, if the net assets of the partnership are accounted for by the general partner less than the following amount:

(1) Trigger point 1: Total contribution of Class A capital contribution + Total contribution of Class A capital contribution

It is regarded as the “trigger point loss†of the partnership, and the partnership enterprise should enter the liquidation procedure. Triggering point loss to the partnership: First, the general partner and the C-type limited partner bear the loss liability for the property share of the partnership; secondly, the property corresponding to the total investment of the category B by the limited partner of the AB category The share bears the responsibility for loss; again, the limited liability partner of the AB class bears the loss liability for the share of the property corresponding to the total contribution of the Class A.

(2) Trigger point 2: The basic income of the total investment of category B + total contribution of category B

It is regarded as the “trigger point loss†of the partnership, and the partnership enterprise should enter the liquidation procedure. Trigger point loss to the partnership: First, the general partner and the C-type limited partner bear the loss liability for the share of the property they enjoy in the partnership; secondly, the AB-type limited partner is in the partnership when they withdraw from the partnership. The share of the property bears the responsibility for loss.

7. Statement of asset manager and custodian

The asset manager promises to manage and use the assets of the asset management plan in accordance with the principles of due diligence, honesty, and diligence, but does not guarantee that the asset management plan will be profitable or guarantee the minimum income.

The asset custodian promises to safely keep the assets of the asset management plan in accordance with the principles of due diligence, honesty, and diligence, and perform other obligations as stipulated in this contract.

8. The record of the asset management plan and the effective conclusion of the asset management contract

Upon expiration of the initial sales period and in accordance with the conditions for the record of the asset management plan, the asset manager shall hire a statutory capital verification institution to verify the capital within 10 days from the expiration of the initial sales period, and submit the capital verification to the CSRC within 10 days from the date of receipt of the capital verification report. Report and customer data sheet, handle the relevant filing procedures. The customer data sheet should include the name of the principal, the identity document number of the principal, the mailing address, the contact number, the amount of the asset management plan, and other information.

Since the date of written confirmation by the China Securities Regulatory Commission, the asset management plan has been completed, and the asset management contract has taken effect. At this time, the custodian has begun to keep the assets of the plan.

9. Risk disclosure and commitment

This asset management plan investment may face the following risks, including but not limited to:

(1) Market risk

In the operation of this asset management plan, the risk of planned property is brought about due to changes in prices such as interest rates, exchange rates, stocks, commodities, land, and real estate.

(2) Policy legal risk

In the operation of this asset management plan, it may bring risks to the planned property due to violation of national laws and regulations; due to factors such as national fiscal policy, monetary policy, industrial policy, regional development policy, etc., system risks may be brought to the planned property. risk.

(3) Risks of financial regulatory policy changes

During the operation of this asset management plan, such as changes in financial regulatory policies, the asset management plan may not meet the requirements of financial regulatory policies, thereby posing risks to the planned assets.

(4) Planned property cannot be realized risk

When the asset management management plan is terminated (including early termination), the planned property may be partially or completely unrealizable due to the market environment or other reasons, thus posing risks to the planned property.

(5) Credit risk

The financial and operating conditions and solvency of a limited partnership will directly affect the income of the client of the plan, such as the failure of the investment project, or the adverse changes in the operating capacity, financial status and solvency of the limited partnership, which may affect The principal and income of the funds are recovered on time.

(6) Management risk

In the actual operation process, the general partner, asset manager, and asset custodian may be limited to knowledge, technology, experience and other factors that affect their judgment on relevant information, economic situation and investment, and may bring risks to the planned property. At the same time, due to the limitations of the experience, skills and other factors of the general partner, asset manager and asset custodian, the plan may deviate from the collection and judgment of information in the process of investing or managing the planned property. The expected return or risk of loss.

According to China's financial regulatory regulations, the asset managers and asset custodians of the plan are approved by the financial regulatory authorities to engage in the corresponding financial business, and operate and manage in accordance with the relevant laws and regulations, but cannot guarantee that they can be permanently maintained. Financial regulatory conditions. If the above parties are unable to continue to operate the corresponding financial business during the duration of the plan, it may have an adverse impact on the plan.

(7) Liquidity risk

If the asset management plan is not open for participation and withdrawal during the existence period, there is a risk that the asset principal cannot withdraw during the existence period; if the limited partnership enterprise fails to pay the investment principal and income on time, the plan will face the risk of insufficient liquidity. According to the agreement, the administrator uses the idle funds in the escrow account for investment in financial products with low risk and good liquidity. If these investments cannot be realized in time for any reason, the plan will expose the plan to the risk of insufficient liquidity.

(8) Risk of early termination or extension of the plan

The plan period is no more than 48 months. In particular, under the transaction document, the asset manager has the right to terminate the plan in advance if the general partner violates the agreement of the transaction document. If the general partner or partnership violates laws, regulations and departmental rules, it may also cause the asset manager to terminate the plan in advance.

The general partner of a limited partnership has the right to choose to extend the capital and income of the Class AB limited partners for a period of not more than 6 months. Under these circumstances, the principal and income distribution time of the A and B asset management plan share classifications agreed in this plan are postponed accordingly.

(9) Specific risks that may be caused by the investment target of the plan

During the period of the plan, if the economic situation changes, policy adjustments, etc., the income of the limited partnerships declines, the solvency decreases or the income of the investment projects decreases, which may result in the relevant interests of the asset principals not being realized in time, in full, or even entrusted with the loss of funds. Happening.

(10) Other risks

The emergence of force majeure factors such as wars, natural disasters, major political events, and financial market crises, industry competition, agency defaults and other risks beyond the direct control of the asset manager may lead to the loss of planned property.

(11) Risk commitment

The asset manager promises to deal with the plan in the best interests of the plan, carefully manage the plan, continuously analyze the potential risks, strive to prevent and resolve possible risks, and safeguard the interests of the asset principal, but the asset manager does not The promised asset trustee is not subject to loss and does not commit to the minimum income of the asset trustee. If the asset manager manages and uses the planned property in accordance with the agreement of the plan documents and transaction documents, the plan property shall be borne by the planned property of the plan.

If the asset manager violates the agreement between the plan document and the transaction document to manage, use, and dispose of the planned property, resulting in loss of the planned property, the asset manager shall be responsible for compensation for the loss. When the asset manager is insufficiently compensated, the asset truster will bear the responsibility.

Fourth, the purpose of foreign investment and the impact on the company

The board of directors of the company fully demonstrated the investment and believed that under the premise of ensuring the capital requirements such as production and operation, the use of its own idle funds of 10 million yuan to purchase the above special asset management plan products will not adversely affect the company's operations. It is conducive to improving the efficiency and income of idle funds, bringing greater economic benefits to the company and maximizing the interests of shareholders.

V. Documents for reference

1. Resolutions of the 18th meeting of the second board of directors;

2. Debon Innovation Capital Xinghao Capital Starlight Yao 3 (No. 1) special asset management plan asset management contract.

Special announcement.

Henan Sifangda Superhard Materials Co., Ltd. Board of Directors

December 11, 2013

December 11, 2013

Deck Mounted Bathtub Faucet,Deck Mount Tub Faucet,Tub Faucet with Sprayer,Tub Faucet with Hand Shower

kaiping aida sanitary ware technology co.,ltd , https://www.aidafaucets.com